Nada Lanz, 43, was born in Albania, grew up in Rome and moved to Switzerland 15 years ago. After going…

What will be deducted from my employee’s salary if I officially register him/her?

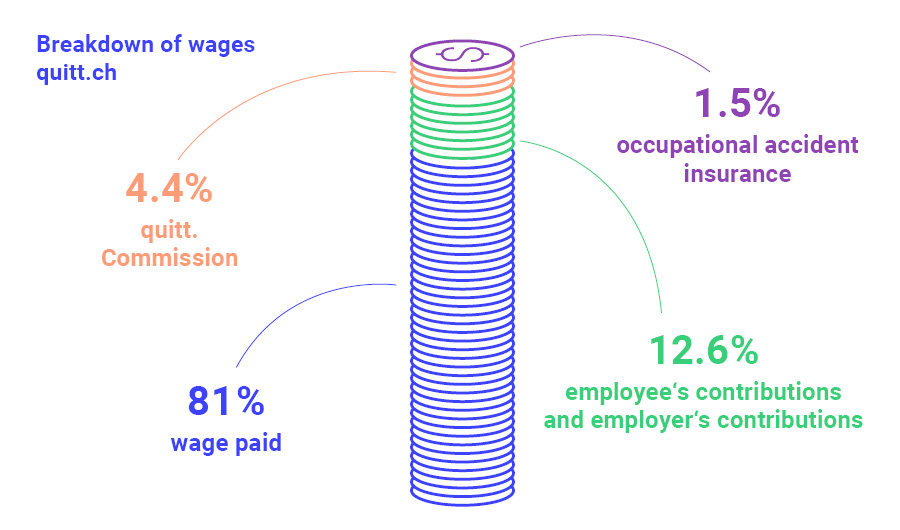

The following contributions will be deducted from your employee’s gross monthly wage, regardless of the amount:

- 5.3% social security deductions (AHV/IV/EO)

- 1.1% unemployment insurance (ALV)

- if necessary, 5% flat-rate tax deduction in the simplified procedure with the compensation office

- if applicable, individual withholding tax according to the tariff notification of the cantonal tax administration

- from CHF 1’837.50 monthly salary individual pension fund (BVG) contributions, the amount of which depends on the employee’s gender, age and salary

If your employee’s gross monthly wage is at least CHF 1’837.50 (or CHF 22’050 annually), the option of lump-sum taxation does not apply any longer. For Swiss nationals and foreigners with a C permit, the tax is then levied normally via the yearly tax return. However, in the case of foreign employees, you as employer are obliged to deduct withholding tax on the gross salary and settle it with the cantonal tax administration.

Employers must pay the same contributions to the relevant compensation office as their domestic help. For the employer, the contributions are also calculated based on the employee’s gross wage. In addition, employers also pay contributions to the family equalization fund (FAK) and administrative costs to the compensation office. Both contributions differ from canton to canton.

On the basis of the data we receive from you as an employer during registration for our service, quitt knows which social contributions, pension fund contributions or withholding tax are relevant to your employment relationship. These contributions are deducted as part of payroll accounting and settled with the relevant authorities at the end of the year. All pay slips are available for download in your personal customer area.

Ähnliche Beiträge